COVID-19 emerged as the turn of the century's Black Swan with a major macroeconomic influence in India and globally.

The exponential spread of COVID-19 has led to a significant decrease in major indicators that have a significant influence and possibility of GDP growth. Although COVID-19 will have a generally negative effect on credit growth in most sectors, the degree and the magnitude of the impact will probably differ depending on the duration and extent of the disruption.

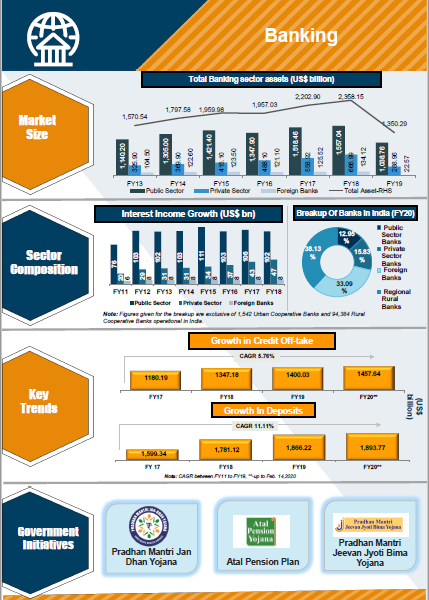

The Indian banking system consists of 20 public-sector banks, 22 private-sector banks, 44 foreign banks, 44 regional rural banks, 1,542 urban cooperative banks, and 94,384 rural cooperative banks, in addition to cooperative credit institutions. The number of ATMs in India was up to 210,263 on January 31 2020 and is expected to rise to 407,000 by 2021 further.

The assets of public sector banks amounted to Rs 72.59 lakh crore ( US$ 1,038.76 billion) in FY19. As per the Union budget 2019-20, the bank coverage ratio has reached the highest in 7 years. As per the Reserve Bank of India ( RBI) as of March 13, 2020, India had foreign-exchange reserves of approximately US$ 481.89 billion.

In the FY16-FY20 period, the credit off-take increased by 13.93 percent to the CAGR. As of FY20, the total extended credit amounted to US$ 1,936.29 billion.

In FY16–FY20, deposits increased by 6.81% to CAGR and by FY20 amounted to US$ 1.90 trillion. Non-food credit increased by 3.3 percent to Rs 89.1 billion (USD 1.26 trillion) on February 28, 2020, and Rs 100.80 lakh crore (USD 1.42 trillion) on March 13, 2020.

Indian banks are increasingly focusing on an integrated approach to risk management. NPAs (Non-Performing Assets) of commercial banks have recorded a recovery of Rs 400,000 crore ( US$ 57.23 billion) in FY19, the highest in the last four years.

According to the Union budget for 2019-20, investment-driven growth required access to low-cost capital, which would require an investment of Rs 20 lakh crore.

Short-term disruption is likely to lead to concerns about the accessibility and scaling-down of SME / corporate customers.

A more prolonged crisis is likely to increase customer preference for digital channels and products such as insurance, in addition to defaults on the part of SMEs / corporate.

A full-blown pandemic is likely to lead to a significant reduction in demand from small and medium-sized enterprises/businesses, structural shifts in customer behavior, and transformation of the role of employees and the overall operating model.

Investors started withdrawing their money. The world's stock markets have crashed. Central banks have made off-cycle rate cuts and injected liquidity to keep the economy moving.

India's NBFCs are facing liquidity tightening after the IL&FS crisis. Banks have been an important source of liquidity for NBFCs, and any weakness in bank deposit financing can constrain the liquidity available to the shadow banking sector.

Many corporate companies cut down the salary and even private banks cut the perks and benefits for their employee. There are many organizations they lay off their employee because of this coronavirus. In terms of Banking sector jobs, there is no such notification of cut down of jobs or layoff for employees.

Coronavirus-related concerns are likely to exacerbate difficulties for Indian banks, Ratings Agency Fitch said, by notching down the operating environment score for the critical sector.

The Agency noted that the outbreak of COVID-19 raises concerns for the sector, which is already reeling under weak business and consumer confidence.

The outlook for the score is "negative" given the uncertainty surrounding the severity and duration of the pandemic and the associated impact of economic activity restrictions on Indian banks.

The operating environment score was last revised down in 2019 due to a weakness in business and consumer confidence, it said.

The lockdown will have an impact on industrial production and domestic demand, it said, adding that it will exacerbate the economic slowdown of the last few quarters, partly due to the weaker availability of credit from non-bank lenders as of September 2018.

If you are at work or are looking forward to resuming work after the pandemic, know that the essence of the job is likely to be very different over the next few years. People who are wary of their health may not give up on social distance soon, and businesses that have survived the COVID will not give up on their knowledge of the crisis. What can you expect once the crisis is over or manageable?

SSC CGL 2020 - general awareness is one of the most scoring sections but many candidates choose to give less importance to it since most of their time

SSC Preparation Strategies & S

1551 followers

The number of aspirants every year attempts for Government exams like SSC CGL. But only some of them are able to crack it. The ratio is relatively low

265 followers

मानव संसाधन विकास मंत्रालय (एमएचआरडी) का नाम बदलकर शिक्षा मंत्रालय कर दिया गया है. प्रधानमंत्री नरेंद्र मोदी की अध्यक्षता में कैबिनेट की बैठक के दौरान

13 followers

UPSC, SSC, IAS, BANKING, DEFENCE, RAILYWAY और अन्य सरकारी और प्रतियोगी परीक्षाओं की तैयारी करने वाले अभ्यर्थी दैनिक करंट अफेयर्स 2020 के अपडेट यहां पढ

2091 followers

Do you think you can not earn while you learn at home in the times of Corona? Think again! Study24x7 is excited to bring to you a unique opportuni

1253 followers

UPSC, SSC, IAS, BANKING, DEFENCE, RAILYWAY और अन्य सरकारी और प्रतियोगी परीक्षाओं की तैयारी करने वाले अभ्यर्थी दैनिक करंट अफेयर्स 2020 के अपडेट यहां पढ

2091 followers

India-Nepal Lipulekh Pass dispute: नेपाल ने अपना नया नक्सा बनाया है जिसमें भारत के तीन क्षेत्र कालापानी, लिपुलेख और लिम्पियाधुरा को शामिल किया गया है.

30 followers

सऊदी अरब अमीरात (यूएई) ने हाल ही में जापान के सहयोग से मंगल ग्रह पर अपना अपना पहला इंटरप्लेनेटरी होप प्रोब मिशन शुरू किया. यूएई का मंगल ग्रह के लिए

30 followers

Copy Link

Copy Link